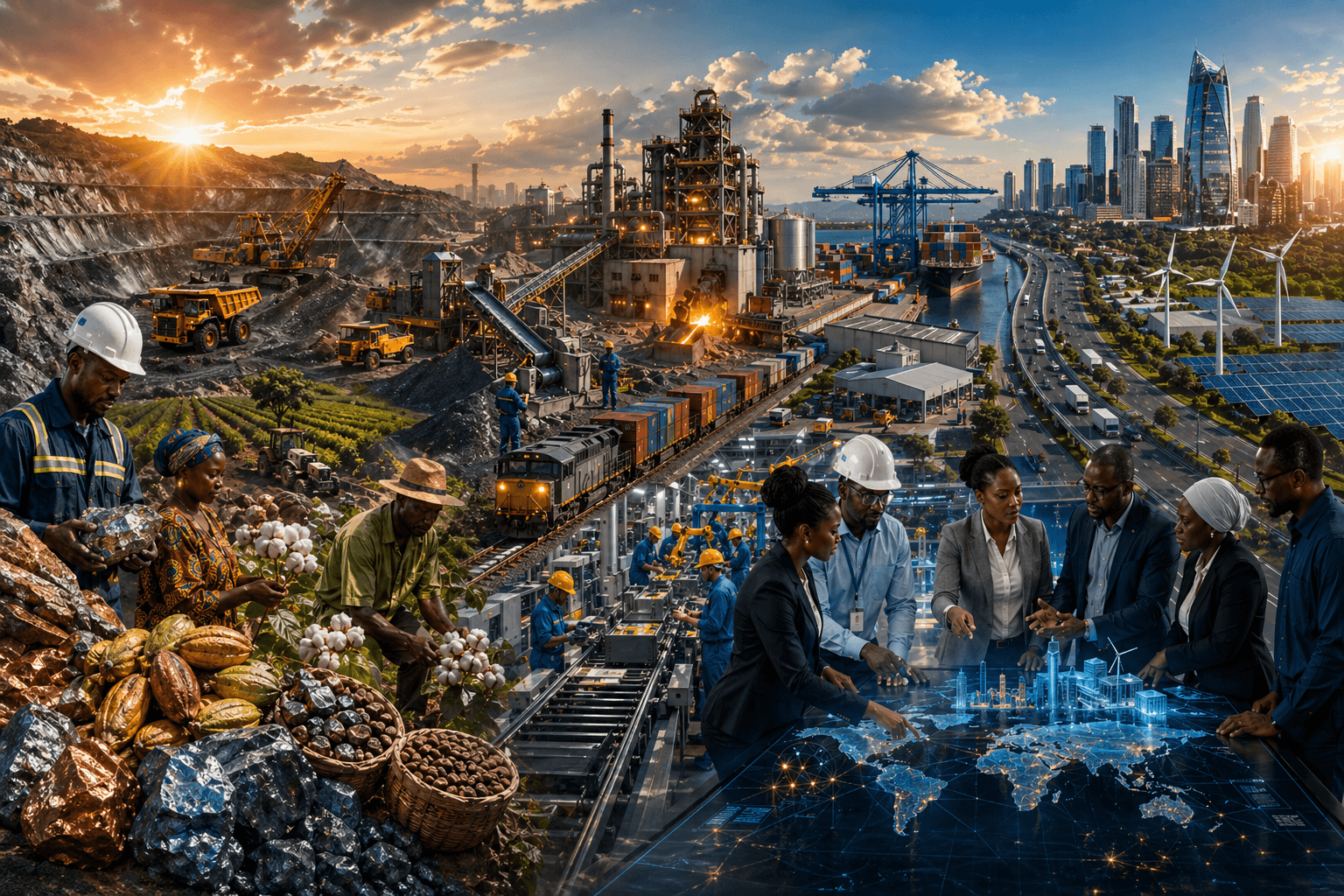

Africa’s future will not be secured by owning resources alone. It will depend on who processes them, manufactures from them, ships them, finances them, and profits from the value chain.

Publication Date: April 27, 2026

By Peter Grear with AI assistance

China’s rise shows that real industrial power does not come merely from possessing raw materials or cheap labor. It comes from building the systems that turn inputs into higher-value goods, national firms, infrastructure, exports, and strategic leverage. Africa now faces that same test. UNECA says AfCFTA can help drive industrialization, agro-processing, and movement up global value chains, while recent UNECA and UNIDO reporting points to the urgency of moving beyond raw commodity exports toward interconnected regional value chains and stronger manufacturing capacity.

For generations, Africa has supplied the world with what it needs while too often importing back what it makes. The continent exports minerals, agricultural commodities, and energy inputs, yet much of the real value is captured elsewhere. The raw material may begin in Africa, but the processing, manufacturing, branding, logistics, and finance are often controlled outside it. That is not just an economic inconvenience. It is one of the central reasons Africa remains structurally underpowered in the global economy.

If Africa is serious about industrialization, that pattern has to change.

China offers a powerful lesson here—not because Africa should imitate China line for line, but because China demonstrates what happens when a country moves from supplying inputs to controlling more of the ladder. China did not become a global industrial force simply by having labor, land, or ambition. It became powerful by building the capacity to transform raw inputs into finished value at scale. Over time, it linked infrastructure, manufacturing, export systems, supplier networks, and domestic firms into one expanding industrial ecosystem. The World Bank has described China’s post-1978 economic transformation as “meteoric,” reflecting how deeply production was woven into national development.

That is the lesson Africa must absorb now: raw materials do not create real power on their own.

A country or continent can own bauxite, cobalt, lithium, cocoa, copper, oil, cotton, or rare earths and still remain economically subordinate if others dominate the profitable stages that come after extraction. The wealth is not only in what comes out of the ground. It is in what happens next. It is in processing, refining, assembling, transporting, insuring, packaging, marketing, financing, and selling into final markets. The side that controls more of those steps controls more of the future.

Africa knows this reality well. For decades, the continent’s place in the global economy has been heavily shaped by extraction. That model has generated income, but it has also left economies exposed to price swings, commodity dependence, weak domestic linkages, and limited job creation relative to the value leaving the continent. UNECA’s Economic Report on Africa 2025 argues that Africa needs structural transformation and stronger productive capacity, and frames AfCFTA as a vehicle for industrialization, agro-processing, and movement up value chains rather than continued dependence on raw commodity exports.

This is why industrialization cannot be understood narrowly as “more factories.” Industrialization is really about value capture.

A continent that mines critical minerals but does not process them is vulnerable. A continent that grows agricultural commodities but does not build agro-processing capacity remains dependent. A continent that hosts extraction but lacks strong logistics, supplier development, and financing systems will continue to watch others climb the value ladder first. China’s rise makes this painfully clear. What changed China’s position was not only that it produced more. It produced differently. It moved deeper into the chain.

Africa now has an opening to do the same in its own way.

The timing matters. Global supply chains are shifting. Governments and firms are reassessing how strategic goods are sourced, where processing takes place, and how economic resilience should be built. Africa is central to that conversation because it holds many of the inputs needed for the energy transition, urbanization, food production, and industrial manufacturing. But importance alone is not power. Africa’s role in future supply chains will depend on whether it remains primarily a source of raw inputs or becomes a stronger site of value-added production.

Recent reporting suggests the opening is real, even if the work ahead is large. The World Bank projects Sub-Saharan Africa’s growth to strengthen from 3.5 percent in 2024 to 3.8 percent in 2025 and to average 4.4 percent in 2026–27, while UNIDO reported that Africa led regional manufacturing growth in the third quarter of 2025. Those numbers do not prove industrial transformation, but they do show that the continent is not standing still.

Still, growth is not enough. Growth without structural change can leave the old dependency model intact.

That is where the harder industrial lesson begins. China did not simply export more raw material. It built industrial zones, transport links, supplier ecosystems, and firms that could absorb larger portions of production and value creation. Africa’s version of that lesson will likely be more regional and decentralized, but the principle is the same: the closer Africa gets to the profitable layers of production, the stronger its economic position becomes.

AfCFTA matters because it can help make that shift commercially viable. Many African countries on their own have limited market size or incomplete industrial ecosystems. But connected through continental trade, regional corridors, and sector-specific value chains, they can build scale together. UNECA has emphasized that Africa must build interconnected regional value chains and move beyond raw commodity exports if AfCFTA is to become transformational rather than symbolic.

This is also where RoFR deserves serious attention.

If RoFR—Right of First Refusal—is designed around strategic sectors, procurement, processing rights, industrial land, logistics contracts, and supplier opportunities, it can help Africans and the diaspora move from watching value chains to entering them earlier. RoFR is not a substitute for industrial policy, infrastructure, or finance. But it can be one of the mechanisms that prevents Africans from being invited into opportunity only after the most valuable positions have already been allocated elsewhere.

In practical terms, that matters enormously. If a major mineral project is launched, who gets the first chance to bid on downstream processing? If a new logistics corridor emerges, who gets first-position access to supply and service contracts? If industrial parks, special economic zones, and trade platforms expand under AfCFTA, who gets the earliest commercial foothold? Those are not side questions. They are central questions of economic power.

The diaspora has a role here too. Too often, diaspora capital is discussed mainly in terms of remittances or sentimental return. But if Africa is to turn raw materials into real power, it will also need engineers, investors, operators, manufacturers, trade specialists, logistics professionals, and policy advocates who can help build value-added systems. RoFR could help create more structured entry points for that participation, especially if tied to regional industrial priorities rather than narrow one-off deals.

None of this means Africa should try to become China. Africa’s path will be different—more distributed, more regional, and more continentally networked. But the deeper lesson still holds. Real power comes not from owning the beginning of the chain, but from climbing it.

Africa has the resources. It has the strategic relevance. It has the growing market. It has the youth. It has the diaspora. What it needs now is a stronger commitment to value capture, industrial depth, and first-position participation.

Because raw materials can make others rich.

Real power comes when Africa builds from them itself.

Donate to GDN – Greater Diversity News | Subscribe – Greater Diversity News

Join the conversation—leave your take or a question.

Help grow The Economic Liberation of Africa conversation—forward to someone curious about Africa-centered opportunity.